TL;DR:

- Manual cross-border payments are costly, slow, and prone to errors and compliance risks.

- Automation can reduce costs by up to 97%, speed up processing times, and improve compliance.

- Effective automation requires strong governance, clear policies, and ongoing exception management.

Manual cross-border payments are quietly draining your business. Each invoice processed by hand can add $8.50 in costs, and that figure doesn’t include the time lost chasing approvals, reconciling mismatches, or fixing compliance errors that slip through during peak periods. For SMEs managing international transactions, these inefficiencies compound fast. This guide breaks down exactly why business payment automation has shifted from a “nice to have” to a genuine operational priority, and how finance and operations managers can use it to cut costs, reduce risk, and stay ahead of regulatory demands without sacrificing control.

Table of Contents

- What drives the need for business payment automation?

- How automation addresses major pain points

- Boosting compliance with smarter payment workflows

- Trade growth and what SMEs need to watch out for

- Why the push for “100% automation” can backfire for SMEs

- Start streamlining your business payments today

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Saves time and money | Automating business payments can cut costs and reduce manual workloads dramatically. |

| Improves compliance | Smart automation slashes false positives and keeps cross-border payments legally sound. |

| Scales international trade | SMEs boost international transaction speed and lower fees, growing global business efficiently. |

| Needs human oversight | Even with automation, expert review and clear escalation policies are vital, especially as payment volume grows. |

What drives the need for business payment automation?

Growing volumes of cross-border transactions expose every weakness in a manual payment process. The pain is real and measurable: high transaction fees, multi-day settlement windows, inconsistent currency conversion rates, and compliance requirements that vary by country and payment corridor.

Manual payment processes also introduce a compounding risk that many finance managers underestimate. When one person processes dozens of supplier invoices per week, small errors like duplicate entries, wrong account numbers, or missed approval steps become statistically inevitable. As payment volume grows, so does the surface area for mistakes.

Common pain points in manual cross-border payment operations:

- High per-transaction banking fees that erode margins on smaller payments

- Settlement delays of 3 to 5 business days for international transfers

- Inconsistent documentation requirements across different countries

- Manual reconciliation that consumes hours of finance staff time every week

- Compliance gaps when sanctions screening or AML checks are done informally

One underappreciated issue is what happens to exceptions at scale. Exceptions grow significantly when automation lacks the supporting evidence it needs, such as purchase orders, contracts, or pre-approved vendor records, and when organizations haven’t defined clear decision policies for non-standard transactions.

“The transition from manual to automated payment processing isn’t just a technology upgrade. It’s an operational reset that forces businesses to document and standardize workflows they’ve been handling ad hoc for years.”

Leading fintechs and cross-border payments platforms are addressing these challenges through tighter integration between payment execution, compliance checks, and financial data management. Rather than treating payments as a standalone task, the smartest platforms treat them as a data-rich workflow where every step generates structured, auditable records. This is also why professional automation use has become standard practice in high-volume financial operations: consistency at scale requires systems, not just skilled people.

How automation addresses major pain points

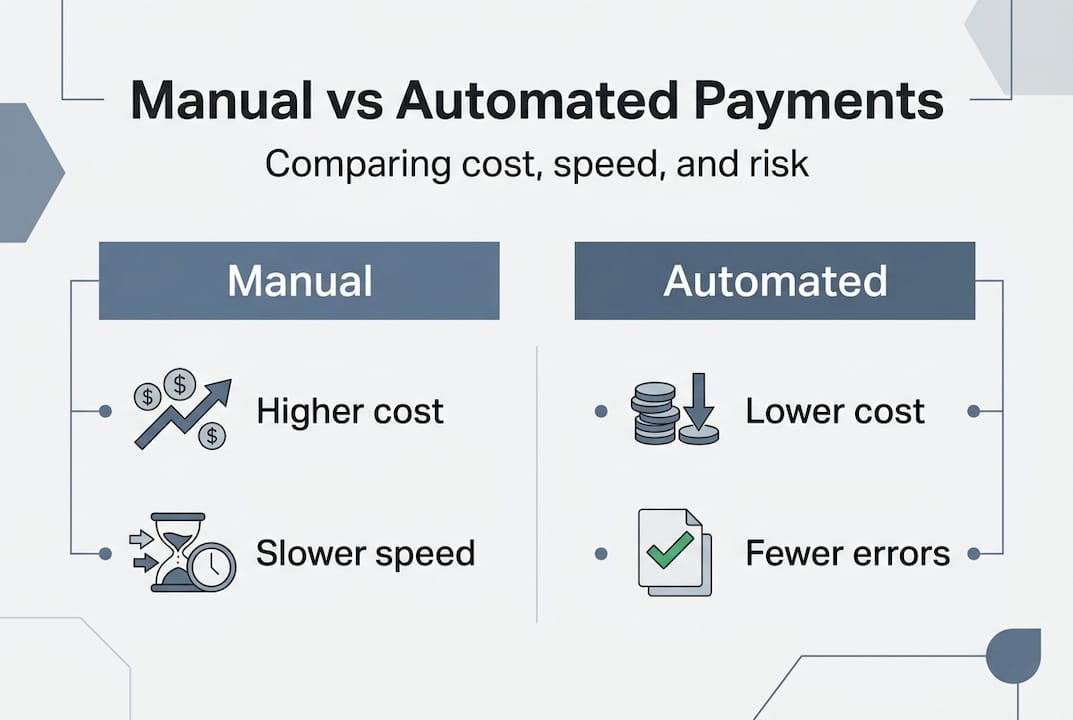

Numbers tell the clearest story here. When organizations move from manual invoice processing to automated workflows, the cost improvements are dramatic. Cost reductions range from 45 to 97% per invoice, dropping from $8.50 down to as little as $0.20 in high-volume automated environments. Even a conservative 45% reduction meaningfully changes the unit economics of accounts payable for a business processing hundreds of invoices per month.

Processing speed improves just as dramatically. Documented case studies show 62 to 82% cycle time reductions alongside FTE (full-time equivalent) savings of two or more staff members and over 320 hours per month freed from manual data entry and reconciliation work. That’s labor that can be redirected toward supplier negotiation, cash flow forecasting, or strategic financial planning.

How manual and automated payment processes compare:

| Metric | Manual process | Automated process |

|---|---|---|

| Cost per invoice | $7.00 to $8.50 | $0.20 to $3.20 |

| Processing time | 5 to 10 days | 1 to 2 days |

| Error rate | 3 to 5% | Less than 0.5% |

| Compliance audit trail | Inconsistent | Automatic and complete |

| Staff hours per 100 invoices | 8 to 12 hours | 1 to 2 hours |

| Exception handling | Ad hoc | Structured and policy-driven |

The efficiency argument for automation is well established, but the operational risk reduction is often what finally moves finance managers to act. Every manual payment step is a potential failure point: wrong beneficiary details, missed approval, or a payment released without the required documentation. Automation removes most of these failure points by design, enforcing rules consistently regardless of workload or staff availability.

How to start automating your SME payment workflow:

- Map your current process. Document every step from invoice receipt to payment confirmation, including who approves what and where data is re-entered manually.

- Identify your highest-frequency payment types. Recurring supplier payments and payroll are ideal starting points because the rules are clear and consistent.

- Define your exception policy. Decide upfront how your system should handle missing POs, payment amount mismatches, or unrecognized vendors before you go live.

- Choose a platform that integrates compliance natively. Platforms that separate payment execution from compliance screening create more work, not less.

- Run a parallel process for 30 days. Let automation process payments while your team verifies outputs, building confidence before fully switching over.

- Review metrics monthly. Track cost per invoice, processing time, exception rate, and error rate to benchmark your gains and tune the system.

Connecting automation to the right banking infrastructure is equally important. A platform built for international payments for SMEs will support SEPA, SWIFT, and multi-currency transactions without requiring your team to manually log into multiple banking portals. Equally, building a secure payment workflow from the start means your automation gains don’t come at the expense of financial controls.

Pro Tip: Start with your three highest-frequency payment types rather than trying to automate everything at once. Quick wins in recurring supplier payments or inter-company transfers build team confidence and generate the ROI data you’ll need to justify broader investment.

Boosting compliance with smarter payment workflows

Compliance in cross-border payments is not a static checkbox. It involves sanctions screening, AML (anti-money laundering) checks, beneficial ownership verification, and country-specific regulatory requirements that can change with little warning. Manual compliance workflows fail here not because people aren’t diligent, but because the volume and complexity of checks exceeds what any team can sustain without errors.

AI-driven automation changes this calculus significantly. AI automates compliance checks, reducing false positives by 40% in cross-border payment environments. False positives, where legitimate transactions get flagged as suspicious and held for manual review, are one of the biggest hidden costs in international payments. Each false positive requires staff time to investigate and resolve, and in volume, they create serious bottlenecks.

Key compliance wins that automation delivers:

- Consistent sanctions screening on every transaction, not just spot checks

- Automatic audit trails that capture timestamps, approver identities, and decision rationale

- Structured record keeping that makes regulatory reporting faster and more accurate

- Reduced manual review queues as AI learns to distinguish genuine risk from noise

- Real-time alerts for transactions that genuinely need human judgment

The compliance table below illustrates typical processing differences between manual and automated systems for a mid-sized SME processing 500 cross-border payments per month:

| Compliance task | Manual processing time | Automated processing time |

|---|---|---|

| Sanctions screening | 2 to 4 hours per day | Near-instant, batch processed |

| AML review | 1 to 3 days per flagged case | Hours, with AI pre-screening |

| Audit trail generation | Manual documentation, 1 hour per case | Automatic, zero additional time |

| Regulatory reporting | 2 to 4 days per quarter | Hours with structured data export |

Staying current on modern banking and compliance trends matters because regulators are not standing still. The direction of travel across EU payment regulation is toward more documentation, faster reporting, and tighter AML obligations. Automation positions you to meet those requirements without proportionally increasing headcount. And as AI in sanctions compliance continues to mature, the gap between manual and automated compliance quality will only widen.

The broader impact of AI in finance automation also extends to predictive flagging, where systems identify unusual patterns before they become compliance incidents rather than after. This is a significant capability shift for SMEs that previously relied on periodic audits to catch problems.

Pro Tip: Set clear escalation procedures before you go live. Document exactly who gets notified when automation flags a transaction it can’t resolve, what the decision timeline is, and how the outcome gets recorded. Without this, automated flags pile up unresolved and create their own compliance risk.

Trade growth and what SMEs need to watch out for

The aggregate impact of payment automation on international trade is substantial. Efficient payment systems boost trade by roughly 4% by lowering the fees and delays that currently discourage smaller businesses from engaging in cross-border commerce. For individual SMEs, faster and cheaper payments mean better supplier relationships, improved cash flow predictability, and the ability to compete with larger players who historically had access to better banking infrastructure.

Fast, reliable payment execution also changes how you negotiate. When your suppliers know payments arrive on schedule and without errors, you gain credibility that can translate into better pricing, extended terms, or priority treatment during supply shortages. These are real commercial advantages, not just operational efficiencies.

What automation genuinely improves for cross-border trade:

- Lower per-transaction fees when using fintech rails versus traditional correspondent banking

- Shorter settlement windows, from 3 to 5 days down to 24 hours or less for SEPA transactions

- Better currency conversion visibility and the ability to lock rates at the time of payment initiation

- Reduced administrative burden when trading with multiple suppliers across different countries

- Stronger audit trails that simplify VAT reclaim processes and cross-border tax compliance

However, the limitations of automation deserve equal attention. Scale requires integrating external evidence and clear governance, and human escalation remains essential beyond pure automation. Early automation wins are often straightforward: standard invoice formats, known vendors, predictable amounts. But as your transaction complexity grows, so does the frequency of edge cases that require human judgment.

“Automation handles the routine brilliantly. The risk is assuming that because the routine is running smoothly, the exceptions are too.”

Knowing how to use SEPA transfer best practices within your automated workflows is one area where operational detail matters enormously. SEPA Instant Credit Transfer, for example, requires correct BIC and IBAN formatting and immediate processing, which means any pre-payment validation errors become immediately visible rather than surfacing days later.

Finance managers scaling cross-border payment automation need to watch three governance areas closely: the completeness of their vendor master data, the clarity of their payment approval hierarchies, and the responsiveness of their exception handling process. Weak governance in any of these areas will limit how much value automation can actually deliver.

Why the push for “100% automation” can backfire for SMEs

Here’s a view you won’t often hear from vendors selling automation software: chasing complete, end-to-end automation without robust governance infrastructure is one of the fastest ways to create new operational problems while solving old ones.

The logic of “automate everything” sounds appealing, especially when the early results are so positive. Costs drop, processing times shrink, errors disappear. But as scale increases, exceptions multiply if your automation system lacks the external evidence it needs to handle non-standard transactions confidently. A vendor invoice that doesn’t match a PO, a payment to a new counterparty in a high-risk jurisdiction, a currency mismatch between the order and the invoice: these all require a decision, and automation needs either perfect data or a clear escalation path to make the right call.

What the best-run SMEs actually do is build automation that’s designed to fail gracefully. When a payment falls outside defined parameters, the system flags it clearly, routes it to the right person with the context they need to decide quickly, and records the outcome so the system can learn from it. This is fundamentally different from automation that either forces through borderline transactions or creates a queue of unresolved flags that nobody owns.

The IBAN account structure matters here too. When your payment infrastructure includes IBAN’s role in payments with multi-account setups and role-based user access, your escalation workflows become far cleaner because the right people have visibility into exactly the payments they’re responsible for, without needing access to unrelated accounts or data.

The bottom line is this: automation is not a destination. It’s a system that requires continuous tuning, regular exception reviews, and honest assessment of where human judgment still adds more value than an algorithm. The SMEs that get the most from payment automation are the ones that treat it as an ongoing operational discipline, not a one-time technology deployment.

Pro Tip: Schedule a monthly exception review where your finance team examines every flagged or manually overridden payment from the previous 30 days. Use that data to update your approval thresholds, vendor policies, and escalation rules. This single habit separates payment automation that compounds in value from automation that plateaus after the first 90 days.

Start streamlining your business payments today

If this guide has highlighted gaps in your current payment workflow, the next step is finding infrastructure that genuinely supports the combination of automation, compliance, and financial control your business needs. Generic banking solutions often lack the multi-account structures, native SEPA and SWIFT support, and role-based access controls that make compliant automation viable for cross-border SME operations.

Demivolt’s business banking solutions are built specifically for businesses that need regulated, digital-first payment infrastructure without the overhead of traditional banking. From dedicated IBAN accounts and segregated client funds to virtual business cards and seamless SEPA and SWIFT integration, Demivolt gives finance and operations managers the tools to automate payments with confidence. Onboarding is fast, transparent, and designed to meet EU regulatory standards from day one, so your automation investments are built on a compliant foundation rather than patched together after the fact.

Frequently asked questions

What is payment automation in business?

Payment automation uses digital tools to schedule, process, and track business payments automatically, reducing manual effort and the errors that come with high-volume, repetitive financial transactions.

How much can SMEs save by automating payments?

SMEs can cut invoice processing costs by up to 97% per invoice and reclaim hundreds of staff hours per month that were previously spent on manual data entry and reconciliation.

How does automation help with compliance in cross-border payments?

AI-driven automation reduces false positives by 40% and accelerates compliance checks across sanctions screening, AML reviews, and audit trail generation, making cross-border transactions safer and significantly faster to process.

Are there risks in automating all business payments?

Yes. Over-automation without supporting governance creates real exposure: exceptions grow at scale when automation lacks the evidence or decision policies it needs to resolve non-standard transactions, which can amplify errors rather than eliminate them.