TL;DR:

- User-based account management controls digital identities throughout their lifecycle, reducing security and compliance risks. Automating processes with tools like SCIM and implementing policies such as RBAC and JIT access improves efficiency and security. Regular reviews and addressing vulnerabilities like orphaned accounts and excessive privileges are essential for effective governance.

User-based account management is defined as the lifecycle governance of digital identities, covering creation, authentication, authorization, monitoring, and deprovisioning across all business systems. The industry standard term for this practice is Identity and Access Management, or IAM, and modern frameworks mandate audit trails and full lifecycle control to prevent unauthorized access. For SMEs and e-commerce businesses, this is not a back-office IT concern. It is the mechanism that determines who touches your financial data, who can approve payments, and who retains access after leaving your organization. NIST SP 800-53 and MITRE ATT&CK both treat user account governance as a primary security control, not an optional configuration.

What is user-based account management and why does it matter?

User-based account management is the structured process of controlling every digital identity inside your organization from the moment an employee joins to the moment they leave. Each account carries permissions that define what systems a person can read, edit, or approve. Without a formal process, those permissions accumulate, overlap, and create gaps that expose financial systems to both internal misuse and external attack.

The core principle is simple: every user gets exactly the access their job requires, nothing more. This sounds obvious, but most SMEs discover they have violated it repeatedly once they audit their systems. A finance assistant who was temporarily given payroll access during a staff shortage three years ago may still hold that access today. That is a textbook example of access creep, and it is one of the most common vulnerabilities in small business environments.

The scope of user account management explained in full includes five stages: provisioning, authentication setup, authorization assignment, ongoing monitoring, and deprovisioning. Each stage carries distinct risks if skipped or handled manually. Deprovisioning is the most neglected. Orphaned accounts from former employees remain a leading cause of security breaches precisely because no one formally closed them.

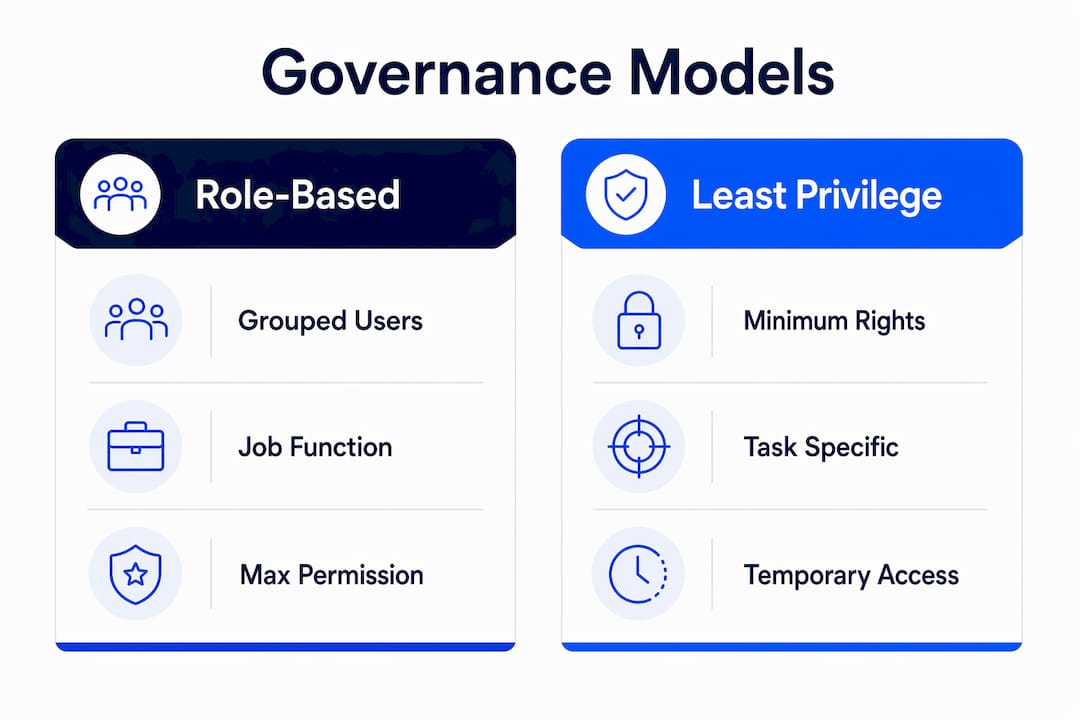

Key principles and frameworks for user account governance

The two foundational models for user account governance are Role-Based Access Control and the Principle of Least Privilege. Understanding both is non-negotiable for any SME managing financial operations.

Role-Based Access Control (RBAC) groups users by job function rather than assigning permissions individually. A payments team member gets access to the payment portal. An accountant gets read access to transaction records. A system administrator gets infrastructure access. RBAC combined with PoLP minimizes financial risk by ensuring no single user holds more access than their role requires.

Principle of Least Privilege (PoLP) takes RBAC further by enforcing minimum necessary access at the permission level. Even within a role, PoLP restricts what a user can do. A finance manager may have read access to all accounts but write access only to accounts within their department.

Three additional principles complete a sound governance framework:

- Separation of duties: No single user should be able to initiate and approve the same financial transaction. This directly reduces the risk of internal fraud in payroll and accounts payable.

- Audit trail requirements: Every access event, permission change, and login attempt must be logged. Compliance frameworks including NIST SP 800-53 AC-2 require automated account auditing as a baseline control.

- Access reviews: Permissions must be reviewed on a scheduled basis, not just at onboarding. Roles change, projects end, and staff move between departments.

Pro Tip: Design role policies with a maximum permission ceiling per role, then require a formal approval process for any exception. This prevents ad hoc privilege grants from becoming permanent fixtures.

How does automation improve user account lifecycle management?

Manual user account administration through spreadsheets and email tickets is not just slow. It is structurally unsafe. When provisioning depends on a human remembering to send a request, and deprovisioning depends on HR notifying IT, accounts get created late and closed never.

Automation solves this through two primary mechanisms. First, SCIM (System for Cross-domain Identity Management) connects your identity directory to every application your team uses. When you add a user in your central directory, SCIM provisions their accounts across all connected systems automatically. Centralized identity management eliminates fragmented spreadsheet tracking and reduces provisioning time from days to minutes. That speed difference matters when a new hire needs payment system access on day one.

Second, lifecycle event triggers automate the right actions at the right moments. The four critical lifecycle events are:

- Onboarding: Accounts are created and permissions assigned based on the user’s role before their start date.

- Role change: When a user moves to a new department, old permissions are revoked and new ones are granted automatically.

- Access review: Periodic automated reports flag accounts with unused permissions or excessive privileges for human review.

- Offboarding: When employment ends, all accounts are deprovisioned within minutes, not days.

The practical benefit for SMEs is significant. A business with 50 employees across finance, operations, and sales can manage access for all of them through a single identity directory rather than logging into each application separately. For financial onboarding best practices, automation is the difference between a compliant process and a compliance liability.

Pro Tip: When selecting a user management platform, prioritize SCIM support and native integration with your banking and accounting tools. Platforms that require manual exports will reintroduce the same delays automation is meant to eliminate.

What security challenges should SMEs know about?

The MITRE ATT&CK M1018 framework identifies user account management as a primary defense mechanism against credential-based attacks. The core insight is that attackers rarely break in. They log in. They use stolen or overprivileged credentials to move through systems undetected. User account management as attack surface reduction reframes the entire practice from IT administration into business security strategy.

Static versus dynamic privilege models

Most SMEs operate on a static privilege model: permissions are assigned at onboarding and rarely changed. Dynamic models replace this with time-limited, task-specific access.

| Feature | Static privileges | Dynamic privileges |

|---|---|---|

| Access duration | Permanent until manually revoked | Time-limited, auto-revoked |

| Risk exposure | High, especially after role changes | Low, minimal persistent access |

| Admin overhead | Low initially, high over time | Higher setup, lower long-term risk |

| Compliance fit | Difficult to audit consistently | Audit-ready by design |

Just-In-Time access is the leading dynamic privilege model. JIT access grants temporary elevated permissions with automatic revocation once the task is complete. An accountant who needs to run a month-end payroll report gets elevated access for two hours, then returns to standard permissions. No persistent admin role exists to compromise.

Non-human identities present an equally serious risk that most SMEs ignore entirely. Service accounts, API keys, and automated scripts often carry excessive privileges because they were configured once and never reviewed. 97% of non-human identities carry excessive privileges, making them a high-value target for attackers who gain initial access to a system. Treat every API key and service account with the same lifecycle rigor as a human employee account.

Pro Tip: Run a quarterly audit specifically for non-human identities. List every API key, service account, and automated credential in your environment, then verify each one is still in active use and holds only the permissions it needs.

How do SMEs and e-commerce businesses apply this in practice?

Applying user account governance in an SME financial environment starts with a role inventory. List every job function that touches financial systems, then define the minimum permissions each role requires. This single exercise typically reveals three to five roles that have been over-provisioned for years.

Implementing RBAC in financial operations protects payroll, accounts payable, and banking access from both internal fraud and external compromise. Separation of duties is the most direct control: the person who creates a payment should not be the person who approves it. This applies equally to a five-person startup and a 200-person e-commerce operation.

For businesses managing cross-border payment compliance, user access governance connects directly to regulatory requirements. EU payment regulations and banking compliance frameworks require documented access controls and audit trails. A business that cannot show who had access to its payment systems during a given period will struggle in any compliance review.

Common pitfalls to address immediately:

- Orphaned accounts: Former employees whose accounts were never closed. Audit these monthly.

- Shared credentials: Multiple users sharing one login. This destroys audit trail integrity and violates most compliance frameworks.

- Excessive admin accounts: Too many users with administrator-level access. Limit admin roles to the smallest possible group.

- Infrequent access reviews: Permissions reviewed annually are effectively never reviewed. Quarterly is the minimum for financial systems.

- Ignoring third-party access: Vendors and contractors who retain access after a project ends carry the same risk as orphaned internal accounts.

For a structured approach to managing multiple accounts across departments, a step-by-step framework prevents the ad hoc decisions that create these vulnerabilities in the first place. The compliance obligations in payments that govern SME financial operations make documented access governance a legal requirement, not just a best practice.

Key Takeaways

User-based account management is the foundational control that determines who accesses your financial systems, and gaps in that control create both security and compliance exposure.

| Point | Details |

|---|---|

| Define roles before assigning access | Build a role inventory first; assign permissions to roles, not individuals. |

| Automate provisioning and deprovisioning | Use SCIM-based tools to eliminate manual delays and orphaned accounts. |

| Apply dynamic privileges where possible | JIT access reduces persistent credential risk in financial and admin systems. |

| Audit non-human identities quarterly | API keys and service accounts carry excessive privileges and are frequently overlooked. |

| Conduct access reviews at least quarterly | Stale permissions in financial systems create compliance gaps and fraud risk. |

The part most SMEs get wrong about account management

The most common confusion I see is between user-based account management and client account management. These are entirely different disciplines. Confusing internal access governance with customer relationship management leads businesses to misallocate resources, treating a security and compliance function as a sales or service function. They are not interchangeable. One governs who inside your organization can touch your systems. The other governs how you manage relationships with customers. Mixing them up means neither gets the attention it deserves.

The second thing most SMEs underestimate is how quickly a clean access structure degrades. You can implement perfect RBAC on day one and have a mess within 18 months if you do not build review cycles into your operations calendar. Access creep is not a failure of technology. It is a failure of process. The businesses I have seen handle this well treat access reviews the same way they treat financial audits: scheduled, documented, and non-negotiable.

Non-human identity management is the blind spot I find most consistently. Every SME I have worked with has API keys and service accounts that no one has reviewed in years. Some belong to vendors who no longer work with the business. Some have admin-level access that was granted for a one-time task. This is not a theoretical risk. It is an open door.

The balance between security rigor and operational usability is real, and JIT access is the best tool I have seen for maintaining it. Permanent admin roles feel convenient until they are compromised. Time-limited access feels like friction until you realize it eliminates an entire category of credential risk. Build the review culture first, then layer in automation. The technology only works if the process behind it is sound.

— dd

Demivolt’s tools for financial access control and compliance

Demivolt supports SMEs and e-commerce businesses that need structured financial account management alongside their banking operations. The platform’s role-based user management and multi-account structure make it practical to apply access governance directly within your financial infrastructure.

For businesses validating payment account details as part of their access and compliance workflows, Demivolt’s IBAN validation tool provides free ISO 13616 verification. The broader SEPA tools suite supports SMEs managing payment operations with the accuracy that compliance frameworks require. Demivolt’s blog resources on multi-account structures for SMEs and fintech onboarding compliance give decision-makers the operational context to apply account governance effectively from day one.

FAQ

What is user-based account management in simple terms?

User-based account management is the process of controlling who gets access to which systems inside your organization, from the moment they join to the moment they leave. It covers account creation, permission assignment, monitoring, and closure.

How does RBAC differ from the Principle of Least Privilege?

RBAC groups users by job role and assigns permissions to that role. PoLP then limits those permissions to the minimum each role actually needs. They work together: RBAC defines the structure, PoLP enforces the ceiling.

Why are orphaned accounts a security risk?

Orphaned accounts belong to former employees or inactive users whose access was never revoked. Attackers can use these accounts to enter systems without triggering alerts, since the credentials appear legitimate.

What is Just-In-Time access and when should SMEs use it?

Just-In-Time access grants temporary elevated permissions for a specific task, then revokes them automatically. SMEs should use it for any admin or financial approval function where permanent elevated access creates unnecessary risk.

How often should SMEs review user access permissions?

Quarterly reviews are the minimum for financial systems. Regular access reviews catch stale privileges before they become compliance violations or security incidents.

Recommended

- Demivolt | Blog – How to manage multiple accounts: A step-by-step guide for SMEs

- Demivolt | Blog – Multi-Account Structure Examples for SMEs and E-Commerce

- Demivolt | Blog – Business account verification: compliance and efficiency for SMEs

- Demivolt | Blog – Multi-account setup process guide for SMEs