TL;DR:

- SWIFT is a secure messaging network, not a funds transfer system, used globally by banks.

- Innovations like SWIFT GPI and SWIFT Go improve speed, transparency, and cost predictability for businesses.

- Compliance checks and intermediary routing cause delays, but SWIFT provides essential proof and trust in regulated trade.

Most businesses assume SWIFT payments work like a wire transfer that zaps money across borders in seconds. That assumption costs time, money, and sometimes deals. SWIFT is not a funds transfer system. It is a secure global messaging network that tells banks what to do with money, and understanding that distinction changes how you manage international payments entirely. For SMEs navigating cross-border trade, supplier payments, or regulated client relationships, SWIFT is often the only credible option. This guide explains exactly how SWIFT payments work, what they cost, where they slow down, and when they are the right tool for your business.

Table of Contents

- What is a SWIFT payment? The essentials

- How SWIFT payments work: Step-by-step process

- Key SWIFT innovations: GPI and SWIFT Go for businesses

- Costs, timing, and alternatives for SMEs

- Common challenges and compliance considerations

- The real value of SWIFT for SMEs: Beyond speed and cost

- Simplify global payments for your business

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| SWIFT is a messaging system | It sends secure payment instructions between financial institutions but does not actually transfer funds itself. |

| Key features for businesses | GPI and SWIFT Go add fast tracking, cost transparency, and low-fee options for SMEs and digital operations. |

| Compare SWIFT with alternatives | Local rails and fintech solutions can be cheaper and faster but lack SWIFT’s universal reach and compliance benefits. |

| Watch for compliance delays | Most delays are due to regulatory checks, cut-off times, and data issues, not the SWIFT system itself. |

| Choose based on need | SMEs should use SWIFT when audit proof, exotic currencies, or regulatory compliance are required. |

What is a SWIFT payment? The essentials

SWIFT stands for Society for Worldwide Interbank Financial Telecommunication. Founded in 1973, it is not a bank and it does not hold or move money. Think of it as a highly secure postal system for financial instructions. When your bank sends a SWIFT message, it is telling another bank to credit a specific account with a specific amount. The actual funds move through existing banking infrastructure, not through SWIFT itself.

The scale is staggering. SWIFT connects 11,000+ institutions across more than 200 countries, processing over 44 million messages every single day. That reach is why SWIFT remains the backbone of international business payments, even as fintech alternatives have grown rapidly.

Every SWIFT payment relies on a BIC (Bank Identifier Code), also called a SWIFT code. This is an 8 or 11 character code that identifies the recipient’s bank precisely. Without it, the message cannot be routed correctly. Here is what a standard SWIFT payment instruction includes:

- Sender’s BIC/SWIFT code and account details

- Recipient’s BIC/SWIFT code and account number or IBAN

- Amount and currency

- Payment purpose or reference

- Correspondent bank details (when applicable)

A common misconception is that SWIFT payments are only for large corporations or financial institutions. In practice, any business with a bank account can initiate a SWIFT payment. The network is universal by design.

| Feature | SWIFT | Local bank transfer |

|---|---|---|

| Global reach | 200+ countries | Usually domestic |

| Proof of payment | MT103 document | Varies by bank |

| Compliance checks | Mandatory at each hop | Minimal |

| Typical speed | 1 to 5 days | Same day or next day |

| Use case | Cross-border, regulated | Domestic, high-volume |

As Stripe’s SWIFT explainer notes, the real value of SWIFT is not speed. It is standardization and trust. When a regulated client or overseas supplier asks for an MT103, they are asking for proof that a compliant, traceable instruction was sent through a globally recognized network. That proof matters in trade, legal disputes, and audits.

“SWIFT does not move money. It moves the instructions that tell banks how to move money.” This distinction is the foundation of every international payment strategy worth building.

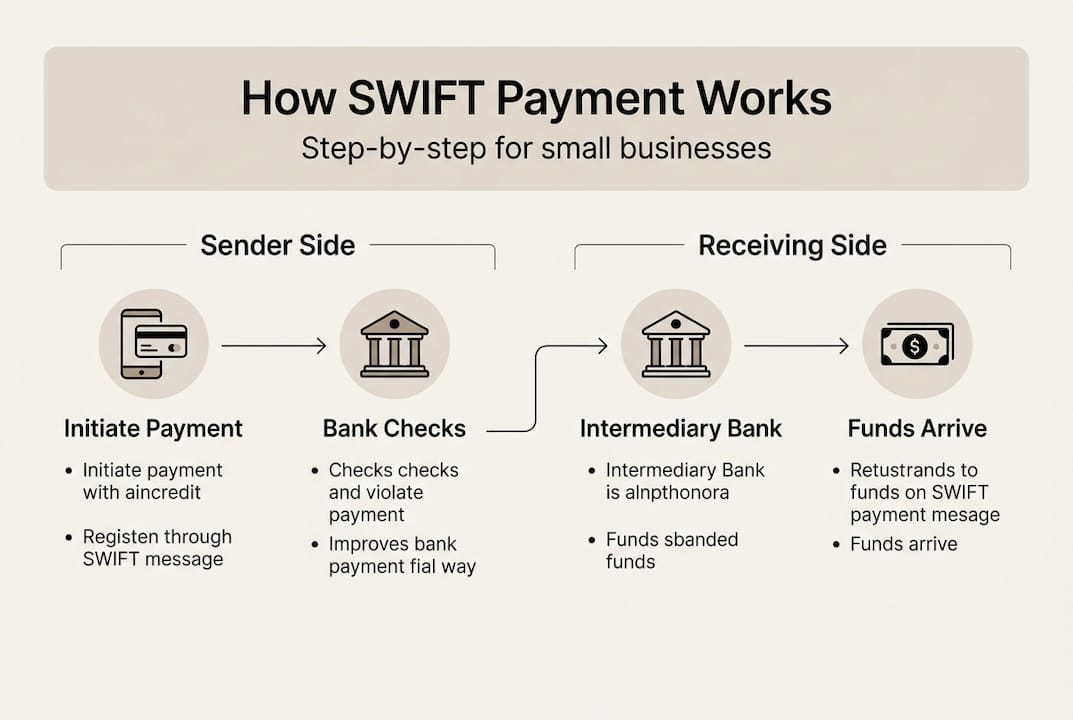

How SWIFT payments work: Step-by-step process

Understanding the mechanics helps you anticipate delays and avoid costly errors. Here is how a SWIFT payment travels from your account to a supplier overseas.

- You initiate the payment through your bank or business banking platform, providing all required details including the recipient’s SWIFT/BIC code.

- Your bank creates an MT103 message, the standard single customer credit transfer format used in SWIFT’s standardized messaging system.

- The message is sent to a correspondent bank if your bank does not have a direct relationship with the recipient’s bank. This is where most of the routing complexity lives.

- Correspondent banks relay the message, sometimes through one, two, or even three intermediary banks depending on the currency corridor.

- The recipient’s bank receives the instruction and credits the account, after completing its own compliance checks.

- Settlement occurs through central bank systems or nostro/vostro accounts held between correspondent banks.

The correspondent banking layer is what surprises most SME owners. Your payment from London to Jakarta may pass through New York and Singapore before reaching its destination. Each hop adds time and potentially a fee.

| Payment route | Typical intermediaries | Estimated time |

|---|---|---|

| US to EU (major currencies) | 0 to 1 | 1 to 2 days |

| EU to Southeast Asia | 1 to 2 | 2 to 4 days |

| Any to emerging market | 2 to 4 | 3 to 5 days |

Compliance checks at each bank are not optional. Anti-money laundering (AML) screening, sanctions list verification, and transaction monitoring all happen at every node in the chain. If any data field is incomplete or mismatched, the payment can be held or returned.

Exploring the advantages of SWIFT for SMEs becomes much clearer once you see this chain. The network’s strength is also its friction point. Speed is traded for reach and compliance.

Pro Tip: Always double-check the recipient’s SWIFT/BIC code before sending. A single wrong character routes your payment to the wrong institution, and recovering it can take weeks and cost additional fees.

For a practical breakdown of the routing logic, Razorpay’s SWIFT payment guide walks through real corridor examples that are useful for SME planning.

Key SWIFT innovations: GPI and SWIFT Go for businesses

The traditional SWIFT process frustrated businesses for years. Payments disappeared into a black box, fees were deducted without notice, and tracking was nearly impossible. Two major innovations changed that.

SWIFT GPI (Global Payments Innovation) launched in 2017 and fundamentally upgraded the experience. Every GPI payment gets a Unique End-to-End Transaction Reference (UETR), a tracking code that lets you follow your payment in real time across every correspondent bank. Fees are disclosed upfront. Banks commit to same-day processing within their time zones.

The results are measurable. SWIFT GPI tracking and speed show that 75% of GPI payments reach destination banks in under 10 minutes. Full account crediting may still take longer due to local processing, but the visibility is transformative for businesses managing cash flow.

SWIFT Go is designed specifically for lower-value payments, typically under $10,000. It targets the exact use case many SMEs have: paying freelancers, small suppliers, or service providers overseas. Key features include:

- Flat, predictable fees typically ranging from $5 to $15 per transaction

- Speed commitment: 90% of payments credited within 3 hours

- No surprise deductions from intermediary banks

- Full transparency on exchange rates and charges

For SMEs sending frequent smaller international payments, SWIFT Go for small payments represents a genuine step forward. The combination of speed and cost predictability removes two of the biggest pain points in cross-border payments.

Pro Tip: If your business regularly sends payments under $10,000 internationally, ask your bank or payment provider whether they support SWIFT Go. The fee savings and speed improvements add up quickly across dozens of monthly transactions.

For businesses wanting integrated business SWIFT solutions, GPI and SWIFT Go are now the baseline expectation, not a premium add-on.

Costs, timing, and alternatives for SMEs

The total cost of a SWIFT payment is rarely what it appears on the surface. Your bank may charge a sending fee, the correspondent bank may deduct its own fee from the principal, and the exchange rate applied often includes a margin. SWIFT fee benchmarks show that total costs typically run $10 to $50 in bank fees plus a foreign exchange markup of 2% to 5%, with intermediary deductions on top.

| Cost component | Typical range |

|---|---|

| Sending bank fee | $10 to $30 |

| Correspondent bank fee | $5 to $20 per hop |

| FX markup | 1% to 5% |

| Receiving bank fee | $0 to $15 |

Fintech alternatives such as Wise, Airwallex, or local payment rails often cut these costs by 40% to 75% in major corridors like USD/EUR or GBP/AUD. They are faster for routine, high-volume payments between major economies. But they come with real limitations:

- Limited reach in emerging or exotic currency corridors

- No universally accepted proof of payment (no MT103 equivalent)

- Regulatory status varies by jurisdiction

- Not always accepted by regulated counterparties

“Cheaper is not always better. For cross-border payments where proof, compliance, or exotic currencies matter, SWIFT is not a cost. It is an investment in certainty.”

For SMEs managing global payment solutions, the practical answer is a hybrid approach. Use SWIFT where legal proof, regulated corridors, or unfamiliar currencies are involved. Use fintech rails for high-volume, routine payments in major currency pairs where speed and cost matter more than documentation.

Delays are common and usually traceable to specific causes: compliance screening at one of the intermediary banks, cut-off times missed by hours, or a correspondent bank that has not yet adopted GPI standards.

Common challenges and compliance considerations

Even with GPI tracking, SWIFT payments face real-world friction that catches SMEs off guard. Understanding where and why delays happen is the first step to managing them.

The most common delay triggers include:

- AML and sanctions screening at every bank in the chain, not just the first

- Cut-off times: miss your bank’s daily SWIFT window and the payment waits until the next business day

- Non-GPI intermediaries: older correspondent banks that have not adopted GPI still operate as black boxes

- ISO 20022 data mismatches: the new messaging standard requires precise structured data, and errors cause rejections

- Sanctions exposure: if any party in the chain has a sanctions flag, the entire transaction can be frozen

Compliance and AML delays are responsible for the majority of SWIFT payment friction, and up to 80% of final delays happen in the domestic last mile, meaning the recipient’s local banking system, not the international routing.

Pro Tip: Always confirm your bank’s SWIFT cut-off time before initiating a time-sensitive payment. For most European banks, the window closes between 3 PM and 5 PM local time. Missing it by minutes means a full business day delay.

“Compliance is not the enemy of speed. Incomplete data is. A fully populated, accurate SWIFT message clears faster at every checkpoint.”

For businesses managing compliance for international payments, the checklist is straightforward: verify all recipient details before sending, include a clear payment purpose, confirm cut-off times, and maintain records of every MT103 for audit purposes. When a payment is delayed, escalate early and request the UETR tracking reference from your bank immediately.

For more context on how compliance intersects with GPI adoption, trade finance delays with SWIFT offers a useful industry perspective.

The real value of SWIFT for SMEs: Beyond speed and cost

Here is what most fintech marketing gets wrong: it frames SWIFT as a legacy system being disrupted. The reality is more nuanced. Speed and cost are not the only dimensions that matter in international business payments.

For SMEs working with regulated buyers, government entities, or international trade finance, the MT103 is not just a receipt. It is legal proof of a compliant, traceable transaction. No fintech alternative currently offers that universally. SWIFT’s dominance in compliance-heavy corridors is not inertia. It is trust built over five decades of standardized, auditable messaging.

We see businesses make the mistake of switching entirely to cheaper alternatives, then scrambling when a regulated client demands MT103 proof or when a payment to an emerging market fails because the fintech provider simply does not cover that corridor. The smarter play is knowing which tool fits which job. SWIFT for compliance, audit, and reach. Local rails for speed and volume in established corridors. That balance is what international SMEs actually need.

Simplify global payments for your business

Managing SWIFT payments alongside alternative rails, compliance requirements, and real-time tracking is genuinely complex. Most SMEs do not have a treasury team to handle it.

Demivolt’s solutions are built specifically for businesses in this position. The platform supports SWIFT and SEPA payments through dedicated IBAN accounts, with compliance built into the infrastructure. You get transparent fee structures, role-based access for your team, and the kind of regulated, EU-standard banking environment that your international partners and clients expect. If your business is scaling cross-border operations and needs a payment setup that handles both speed and compliance without the guesswork, Demivolt is worth exploring.

Frequently asked questions

How long does a SWIFT payment take?

75% of SWIFT GPI payments reach destination banks in under 10 minutes, but full account crediting typically takes 1 to 5 business days depending on compliance checks and intermediary banks involved.

What information is needed to send a SWIFT payment?

You need the recipient’s full name, SWIFT/BIC code and account number or IBAN, the payment amount and currency, and a clear payment purpose or reference.

Why do SWIFT payments sometimes get delayed?

Compliance and screening delays at each intermediary bank are the most common cause, along with missed cut-off times, non-GPI correspondent banks, or incomplete payment data.

Are SWIFT payments safe for business?

Yes. SWIFT’s 11,000+ institution network operates with mandatory compliance checks, standardized messaging, and robust security protocols, making it one of the most trusted systems for international business payments.