TL;DR:

- Fintech platforms offer faster, cheaper, and more transparent cross-border payments than traditional banks.

- SMEs benefit from reduced fees, same-day settlement, and improved operational efficiency using fintech solutions.

- Regulatory complexity and lack of interoperability remain significant challenges for SME international payment access.

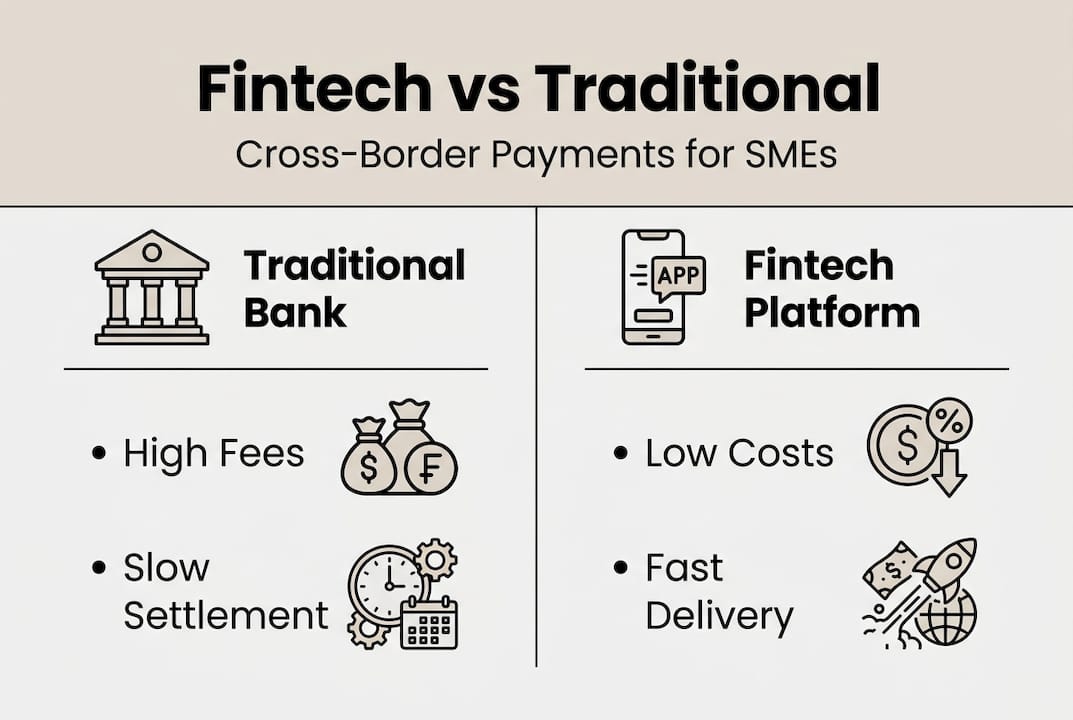

Most SMEs assume international payments work roughly the same regardless of the provider. They don’t. Businesses using legacy banking for cross-border transfers routinely lose 2 to 5% on FX markups plus fixed transaction fees, and then wait several business days for funds to arrive. Fintech platforms have broken that model. By using proprietary networks, multi-currency accounts, local payment rails, and APIs, they move money faster and at a fraction of the cost. If your company is handling any volume of international payments and still relying on a traditional bank, there’s a good chance you’re leaving real money on the table every single month.

Table of Contents

- Why traditional cross-border payments hold SMEs back

- How fintech reshapes global payments for SMEs

- Stablecoins, blockchain, and local rails: Modern fintech in action

- Challenges and regulatory risks for SMEs using fintech

- The missing ingredient: Interoperability and the public-private path forward

- Streamline your cross-border payments with Demivolt

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Fintech cuts payment costs | SMEs can reduce fees from 2-5% (bank) to 0.3-1% using fintech solutions. |

| Faster global transfers | Fintech enables same-day or instant payments, improving cash flow management. |

| Modern rails mean access | Stablecoins and local rails help SMEs reach new markets and underserved regions. |

| Regulatory risks persist | Fragmented licensing and compliance requirements can complicate cross-border fintech use. |

| Interoperability is key | Seamless, connected payment networks and regulation are vital for fintech’s SME impact. |

Why traditional cross-border payments hold SMEs back

The conventional correspondent banking model was built for large financial institutions, not growing SMEs trying to pay suppliers in Vietnam or receive revenue from clients in Brazil. The layers involved are staggering. A single payment can pass through three or four intermediary banks, each one taking a cut and adding settlement delay. By the time funds arrive, the FX rate has moved and the total fees are anything but predictable.

The numbers tell a blunt story:

| Cost element | Traditional banks | Fintech providers |

|---|---|---|

| FX markup | 2 to 5% | 0.3 to 0.8% |

| Transaction fees | $25 to $50 flat | Near zero or minimal |

| Settlement time | 2 to 5 business days | Same-day or faster |

| Fee transparency | Low | High |

Banks charge 2 to 5% FX markup plus $25 to $50 flat fees per transaction, while fintech providers charge 0.3 to 0.8% with same-day settlement. That differential compounds painfully when you’re processing dozens of payments each month.

The structural problem goes deeper than pricing. Correspondent banking has declined 20% since the mid-2000s, cutting off access for many businesses in emerging markets as large banks exit high-risk corridors to reduce regulatory exposure. SMEs, who represent 43% of B2B cross-border flows, feel this contraction most acutely. They don’t have the negotiating power to secure better rates, and they can’t always find a banking partner willing to serve their specific corridors.

Here’s what traditional bank payments actually cost SMEs beyond fees:

- Liquidity strain: Waiting 3 to 5 days for funds to clear ties up working capital your business could put to use immediately.

- FX uncertainty: Rates quoted at the time of initiation may differ from rates applied at settlement, making cash flow forecasting unreliable.

- Opacity: Many banks don’t clearly itemize FX margins separately from fees, making true cost comparison nearly impossible.

- Operational friction: Wiring instructions, SWIFT codes, and manual reconciliation consume finance team hours that could go toward strategic work.

“SMEs aren’t just underserved by legacy banking — they’re actively disadvantaged. The correspondent banking retreat means smaller businesses lose access to the very corridors they need most to compete globally.”

Understanding why the old model fails is the first step. The more useful question is what actually replaces it, and how fintech solutions reshape the fintech payment advantages SMEs can access today.

How fintech reshapes global payments for SMEs

Fintech providers don’t route payments through a chain of correspondent banks. They’ve built alternative infrastructure from the ground up. The core tools include proprietary payment networks that settle between pre-funded accounts, multi-currency wallets that hold balances in local denominations, local payment rails that tap domestic clearing systems in destination countries, and open APIs that connect directly to your accounting or ERP software.

Here’s a practical comparison of what that means in real terms:

| Factor | Traditional bank | Fintech platform |

|---|---|---|

| Cost per international transfer | 2 to 5% + flat fee | 0.3 to 0.8% total |

| Settlement speed | 2 to 5 business days | Minutes to same-day |

| Transparency | Fees often hidden | Real-time rate lock |

| API integration | Rare or complex | Standard feature |

| Multi-currency support | Limited | Built-in |

Fintechs deliver 0.3 to 0.8% cost with same-day or faster settlement, and APIs that automate reconciliation. For an SME sending $100,000 per month internationally, the savings between a 3% bank rate and a 0.6% fintech rate total $2,400 every month. That’s a meaningful budget line.

One increasingly practical technique is the stablecoin “sandwich.” A stablecoin model like Circle’s USDC converts fiat currency to a USD-pegged stablecoin, routes the transfer across a blockchain in seconds, then converts back to local fiat on the receiving end. This approach generates 40% fee savings and near-instant settlement compared to traditional wire transfers. Understanding stablecoin innovations helps SMEs evaluate whether this model fits their payment corridors.

Here’s how a fintech-powered payment flow works in practice:

- You initiate a transfer in your dashboard or via API with a real-time rate lock.

- Your payment routes through local clearing rails or a proprietary network to avoid correspondent banks.

- Funds arrive in the recipient’s account same-day or within hours.

- Your accounting system receives a reconciliation record automatically.

- You see a fully itemized cost breakdown, including the exact FX rate applied.

Pro Tip: If your fintech provider can’t show you the exact FX margin in real time before you confirm a payment, that’s a red flag. Rate transparency is one of the clearest differentiators between serious providers and those still operating with hidden margins.

The modern payment infrastructure built by fintechs also supports automation that legacy banks simply can’t match, from batch payments to real-time FX hedging triggers.

Stablecoins, blockchain, and local rails: Modern fintech in action

Fintech’s cost and speed advantages aren’t magic. They come from applying specific technologies to remove friction at each step of the payment chain. The three most impactful are stablecoins, blockchain settlement, and local payment rails.

The stablecoin sandwich approach works like this: your local currency is converted to a USD-pegged stablecoin (like USDC or USDT), transferred across a blockchain network in seconds, then converted to the recipient’s local currency on the other end. No correspondent bank. No multi-day SWIFT chain. Stablecoin models enable 24/7 instant settlement, with hybrid fiat-stablecoin-fiat approaches best suited to SME needs.

Key benefits for SMEs using this approach:

- 24/7 availability: Blockchain doesn’t close on weekends or public holidays, which matters when you’re trading across time zones.

- Reduced intermediaries: Fewer hops mean fewer fees and fewer points of failure.

- Speed: Blockchain settlement can complete in under a minute for supported corridors.

- Auditability: Every transaction is recorded on an immutable ledger, simplifying reconciliation.

Local payment rails work differently. Instead of routing internationally, the fintech holds pre-funded accounts in multiple countries and settles domestically on both ends. You send euros from Germany, and the recipient in Mexico receives pesos from a local account. The international FX conversion happens inside the fintech’s system, not through your bank’s correspondent network.

Pro Tip: Stablecoin rails work best for established corridors where on-ramp and off-ramp liquidity is deep. For niche markets, local rail solutions typically offer more reliability. Ask your provider which method they use for your specific corridors.

However, emerging market corridors still face challenges around volatility and on/off-ramp liquidity. If you’re transacting in currencies that aren’t pegged to USD, stablecoin conversion introduces temporary exposure. Exploring the details around stablecoin settlement rails helps you identify which approach fits your specific trade flows. For further guidance on SME compliance in payments, the regulatory framework matters as much as the technology.

Challenges and regulatory risks for SMEs using fintech

Adopting fintech for international payments doesn’t eliminate risk. It shifts and sometimes redefines it. The most significant challenge isn’t technology — it’s the regulatory landscape, which varies dramatically by country and is still evolving in response to fintech growth.

Key compliance and regulatory challenges for SMEs include:

- Licensing fragmentation: A fintech licensed in the EU may not be authorized to operate in Southeast Asia or Latin America. Coverage gaps can leave you without a payment option in a key market.

- AML/KYC requirements: Regulatory hurdles including AML/KYC, data localization, and capital controls remain major obstacles for SMEs using fintech in cross-border operations.

- Data localization: Some countries require that financial data be stored on servers within their borders, restricting how global platforms can operate locally.

- Capital controls: In markets like China, Nigeria, or Argentina, government restrictions on currency movement can override your fintech provider’s technical capabilities.

The compliance burden is substantial across the industry. The fintech sector spends around 15% of operating budgets on regulatory compliance, and much of that cost flows downstream to business customers through pricing or service limitations.

“Regulatory fragmentation is the single largest barrier to SME access in cross-border payments. Technology outpaces rules in almost every corridor, but you can only move money where regulation allows.”

On a macro level, G20 targets for retail cross-border payment costs below 1% and 75% of payments completing within one hour are unlikely to be met by 2027, as retail payment friction persists across major corridors. The ambition is right, but implementation is lagging.

SMEs also face corridor-specific risks. High-risk jurisdictions attract fewer fintech providers willing to operate there, and the correspondent banking retreat means fewer fallback options. Understanding national payments alternatives emerging in various markets gives SMEs broader strategic context when building their payment stack.

The missing ingredient: Interoperability and the public-private path forward

Here’s the contrarian take that most fintech coverage skips: the bottleneck holding SMEs back in 2026 isn’t a shortage of technology. There are dozens of capable platforms, well-tested stablecoin rails, and mature APIs. The real problem is that these solutions don’t talk to each other, and neither do the regulators overseeing them.

Standards like ISO 20022 exist to create a common language for payment messages across systems, but adoption is uneven. CBDC bridge experiments between central banks show promise for interoperability, but remain narrow in scope. Bank-fintech partnerships are growing, but interoperability through standards and bank-fintech collaboration is critical — yet implementation consistently lags behind innovation, and public-private cooperation is needed for G20 goals to mean anything in practice.

For SMEs, the practical implication is this: choose providers that actively participate in industry standards bodies and maintain banking partnerships, not just standalone tech stacks. Staying informed about modern banking trends positions your business to benefit when interoperability finally catches up to ambition. The technology is ready. The rails and the rules need to meet in the middle.

Streamline your cross-border payments with Demivolt

If this article clarified how much the payment model has shifted, the next step is putting that understanding to work. Demivolt is a regulated European fintech platform built specifically for businesses that operate across borders. Dedicated IBAN accounts, SEPA and SWIFT payment management, real-time FX transparency, and multi-currency support come standard, with EU-compliant infrastructure and segregated client funds for security.

For SMEs ready to reduce payment costs, improve settlement speed, and gain real financial control, Demivolt’s business banking solutions are worth a close look. If you’re unsure which account structure fits your business, start by exploring how to choose a business bank account that matches your international payment needs. Clarity on your payment infrastructure is one of the highest-return decisions you can make for your business this year.

Frequently asked questions

How do fintech cross-border payments work for SMEs?

Fintech companies use proprietary networks, APIs, and multi-currency accounts to route payments faster and cheaper than legacy banks, often settling in minutes rather than days. This bypasses the correspondent banking chain that drives up costs and delays for traditional wire transfers.

Are fintech cross-border payments secure and compliant?

Most fintech providers comply with AML/KYC and data protection rules, but AML/KYC variations and data localization rules create a complex landscape. Always verify your provider’s licensing in every country where you operate before committing.

Does using fintech save SMEs money versus banks for global payments?

Yes, significantly. Fintechs offer 0.3 to 0.8% total costs with same-day settlement, compared to banks that typically charge 2 to 5% FX markup plus $25 to $50 flat fees per transaction. The savings scale quickly with payment volume.

What risks should SMEs watch out for with fintech cross-border payments?

The main risks include regulatory gaps across jurisdictions, volatility and on/off-ramp issues for stablecoin or crypto rails, and limited access in high-risk or underserved corridors. Vetting your provider’s specific corridor coverage before you rely on them for critical payments is essential.

Recommended

- Demivolt | News – How fintechs facilitate cross-border payments for SMEs

- Demivolt | Blog – International payments for SMEs: efficiency, compliance, growth

- Demivolt | News – How Fintech Platforms Are Transforming Payment Infrastructure

- Demivolt | Blog – Modern business banking trends: boost efficiency & compliance

- SuiteCommerce InStore (SCIS) Payment Integration with Digital Wallets & BNPL

- Why Cloud Accounting Matters: Fuelling Growth for SMEs and Start-ups - Price & Accountants